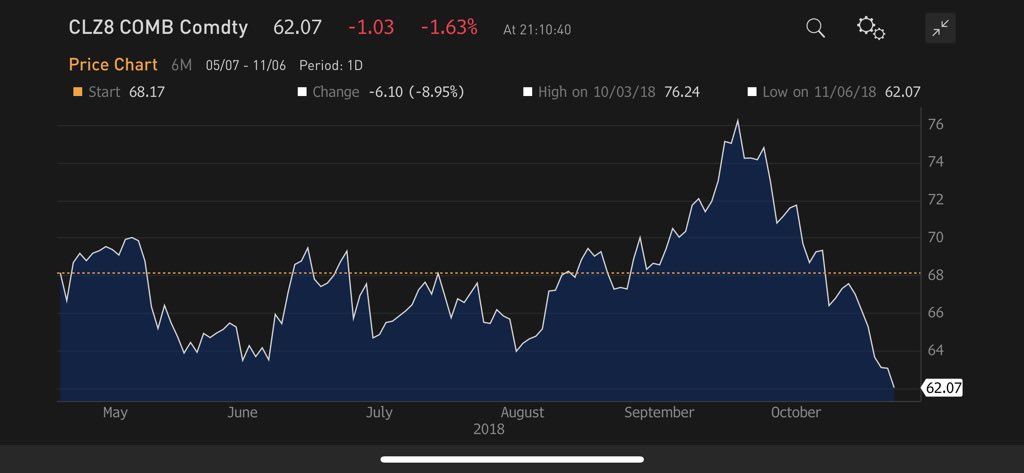

Affascinante davvero, la frenesia quotidiana, l’ansia, è il motore che guida i mercati finanziari e i suoi principali attori, per non parlare del gregge, dove sono finiti i fautori del prezzo del petrolio a 100 dollari al barile?

Non male davvero come performance, passare da 77 dollari a quasi 62, la spettacolare ripresa dell’economia mondiale è andata in fumo nello spazio di un istante!

Difficile fare comprendere ad un gregge di ignoranti il significato profondo di una deflazione da debiti, non c’è nulla da fare, della speculazione che la sostiene, senza il debito l’economia mondiale sarebbe morta e sepolta, perché il secondo denominatore comune di tutte le grandi crisi, l’impressionante, disuguaglianza di ricchezza esistente, non lascia scampo, la madre di tutte le crisi è dietro l’angolo, in un crescendo esponenziale.

In pochissimo tempo il prezzo del petrolio, nell’indifferenza generale è precipitato, disintegrando tutte le medie mobili possibili ai minimi di aprile, si sale per le scale, si scende con l’ascensore e si arriva direttamente nei territori dell’orso nero.

Nel parleremo nel prossimi manoscritto di Machiavelli in dettaglio, ma è chiaro che l’esenzione dall’embargo contro le esportazioni di petrolio dell’Iran concesse a 8 paesi tra cui Italia, Grecia, Turchia, Giappone, Cina, India, Corea del Sud e Taiwan permetterà di continuare ad esportare almeno la metà dello stesso petrolio che esportava prima.

E certo,” per ora “, la carta straccia italiana, non appena vede un successo di questo governo, spera sempre che sia momentaneo, per ora lo spread scende, per ora siamo esentanti dall’embargo, per ora questi pennivendoli sopravvivono, non hanno ancora capito che a differenza dell’Europa possiamo contare sul pieno supporto di Russia e Stati Uniti, Cina compresa.

Credetemi, le fobie sull’inflazione, l’isterismo iperinflativo è una malattia difficile da curare, piano, piano il gregge ci arriverà, noi non abbiamo alcuna fretta!

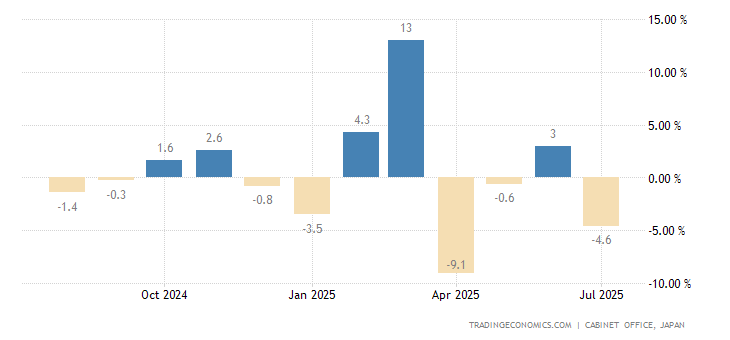

Nel frattempo i maestri della deflazione da debiti, i giapponesi fanno registrare un collasso, di oltre il 18 % degli ordininativi per macchinari a settembre, che porta la dinamica annuale ad un MENO 7 % rispetto ad attese di un aumento dello stesso importo.

I dati assolutamente deprimenti probabilmente porteranno in territorio negativo il prodotto interno lordo nel terzo trimestre.

Un membro della banca centrale giapponese ha dichiarato che la politica monetaria è impotente di fronte al declino strutturale dell’economia giapponese, declino strutturale innestato dalla deflazione da debito.

Studiate la storia della crisi giapponese, capirete molte cose che gli asini, dotti, medici e sapienti, che commentano da anni questa crisi, non capiranno mai.

Stasera c’è la Fed, le solite due chiacchiere al bar tra amici. 8 Novembre 2018 Fonte: qui

LA 39ENNE SAREBBE STATA PICCHIATA DALL’EX COMPAGNO LA SERA PRIMA DELLA SUA SCOMPARSA, PROBABILMENTE DAVANTI AL FIGLIO DI CINQUE ANNI

PER SFUGGIRE ALLE BOTTE LA BELLISSIMA MARIANNA INSIEME AL BAMBINO AVREBBE CHIESTO OSPITALITÀ A UN AMICO. E LÌ AVREBBE ASSUNTO DELLA COCAINA, INSIEME AD ALTRI FARMACI E ALCOL: PROBABILMENTE È STATO PROPRIO QUESTO MIX LETALE A UCCIDERLA...

Due persone sono state iscritte nel registro degli indagati per la morte di Marianna Pepe, la 39enne ex campionessa di tiro a segno. La donna, la sera prima della morte, sarebbe stata violentemente picchiata dall’ex compagno, probabilmente davanti al figlio di cinque anni.

MARIANNA PEPE

Per sfuggire alle botte Marianna insieme al bambino avrebbe chiesto ospitalità a un amico. E lì avrebbe assunto della cocaina, insieme ad altri farmaci e alcol: probabilmente è stato proprio questo mix letale a ucciderla. Sarà comunque l’autopsia a chiarire la causa esatta del decesso. Marianna aveva di recente interrotto il rapporto con l’ex compagno, che però non si rassegnava alla fine della loro relazione. In passato l’uomo era già stato violento, tanto che Marianna si era rivolta al Gruppo di operatrici antiviolenza e progetti (Goap) per chiedere aiuto. Marianna Pepe era stata trovata morta intorno alle tredici di giovedì, a Muggia, vicino Trieste, ma il decesso sarebbe avvenuto nella notte precedente.

È morta in un letto, nella notte tra mercoledì e giovedì. Ma il motivo resta ancora un mistero sul quale sta indagando la Squadra mobile di Trieste. Marianna Pepe, 39 anni, caporalmaggiore scelto dell' Esercito e cinque volte campionessa italiana di tiro a segno nella specialità della carabina sportiva, è stata trovata priva di vita da suo figlio, cinque anni. Erano circa le tredici e quando è arrivata l' ambulanza non c' era più niente da fare.

La donna - che abitava a Muggia, comune vicino a Trieste - era sul letto, attorno non c' erano medicinali e sul cadavere, almeno dopo un primo riscontro medico, non sono stati trovati segni di violenza.

Ma qualcosa non torna.

Dalla Procura di Trieste hanno deciso un approfondimento e per questo è stata disposta l' autopsia prevista martedì. Nel fascicolo non è stata formulata alcuna ipotesi di reato e nemmeno ci sono indagati, almeno sino a quando non giungeranno i risultati dell' esame tossicologico.

MARIANNA PEPE

Per ora ci sono solo ipotesi: forse un malore. O forse un mix letale di farmaci e alcol. A riportarlo è l' edizione online del Piccolo di Trieste che ha ricostruito l' ultima notte di Marianna.

Reduce, tra l' altro, da una relazione sentimentale travagliata e burrascosa con un ex compagno descritto come assai manesco. Ecco perché la donna di recente si era rivolta al Goap («Gruppo operatrici antiviolenza e progetti») di Trieste per chiedere aiuto e fronteggiare quell' uomo incapace di rassegnarsi alla fine di un amore. Mercoledì sera Marianna, che aveva con sé il bimbo, avrebbe deciso di non rincasare proprio per la paura di imbattersi, per l' ennesima volta, nell' ex fidanzato. Per questo si è incontrata con un amico che l' ha ospitata a casa sua, sempre a Muggia. Qui avrebbe assunto dei farmaci, probabilmente del Valium, che mescolato ad alcol sarebbe risultato fatale.

Dalla Squadra mobile diretta da Giovanni Cuciti filtra solo che alcuni familiari e conoscenti dell' ex atleta azzurra sono stati già ascoltati. Su Facebook sono tantissime le testimonianze che ricordano la tiratrice che aveva a lungo indossato la maglia della nazionale.

MARIANNA PEPE

Marianna - bionda, lo sguardo sempre grintoso nelle foto che la ritraggono nelle competizioni - aveva cominciato a sparare, ancora adolescente, in un poligono di Trieste. Le vittorie, numerose, erano arrivate subito, tanto da guadagnarsi l' ingresso nel Gruppo sportivo dell' Esercito di cui era stata atleta in prima fila. Oltre ad aggiudicarsi i cinque campionati era arrivata ottava nella carabina ad aria compressa dai 50 metri, ai campionati europei del 2005.

Dopo aver lasciato lo sport ad alto livello Marianna era entrata nell' Esercito per diventare militare di professione in un reparto a Trieste. Pochi giorni fa aveva sfilato in divisa durante le celebrazioni per il 4 novembre. Poi il mistero di quel che è successo nella notte tra mercoledì e giovedì.

"Morte improvvisa conseguente a insufficienza cardiorespiratoria da edema polmonare secondario a verosimile polintossicazione da diverse sostanze". È la causa della morte di Marianna Pepe, avvenuta l’8 novembre scorso, secondo quanto ha scritto il medico legale che, tra l’altro, "non ha rilevato segni di violenza". Lo riporta una nota della Procura di Trieste che coordina le indagini e che ha già conferito l’incarico per l’autopsia, che sarà svolta mercoledì.

L’autopsia dovrà stabilire se "effettivamente le cause del decesso sono riferibili all’assunzione di sostanze esogene o ad altre cause". In questo senso, "indagini sono in corso per chiarire la responsabilità di chi ha fornito alla donna tali sostanze". La Procura precisa, inoltre, che la famiglia era seguita dai Servizi sociali che sul caso avevano redatto varie relazioni. Si stanno "doverosamente compiendo tutte le indagini per ricostruire i fatti e verificare le responsabilità di ogni soggetto coinvolto", conclude la nota.

MARIANNA PEPE

Sono in corso indagini per chiarire la responsabilità di chi ha fornito a Marianna Pepe, l’ex campionessa di tiro a segno trovata morta a Muggia lo scorso 8 novembre, le sostanze che - stando alle prime ipotesi del medico legale intervenuto sul posto - ne avrebbero provocato il decesso. L’ex compagno di Marianna Pepe, con il quale la donna aveva un figlio, era stato rinviato a giudizio per ipotesi di maltrattamenti.

MARIANNA PEPE

Erano stati riferiti più episodi di violenza, a partire dal 2014, ma la donna aveva poi deciso di ritirare le denunce perché "le violenze erano cessate» e «il compagno aveva mantenuto una condotta collaborativa anche nella gestione del figlio". In una recente telefonata ricevuta dalle forze dell’ordine per accertamenti sulla situazione, la donna aveva riferito, lo scorso 30 ottobre, che la relazione era finita e che il suo ex compagno la rispettava.

Back in 2017, we explained why the "fate of the world economy is in the hands of China's housing bubble." The answer was simple: for the Chinese population, and growing middle class, to keep spending vibrant and borrowing elevated, it had to feel comfortable and confident that its wealth would keep rising. However, unlike the US where the stock market is the ultimate barometer of the confidence boosting "wealth effect", in China it has always been about housing as three quarters of Chinese household assets are parked in real estate, compared to only 28% in the US, with the remainder invested financial assets.

Source: Xinhua

Beijing knows this, of course, which is why China periodically and consistently reflates its housing bubble, hoping that the popping of the bubble, which happened in late 2011 and again in 2014, will be a controlled, "smooth landing" process. For now, Beijing has been successful in maintaining price stability at least according to official data, allowing the air out of the "Tier 1" home price bubble which peaked in early 2016, while preserving modest home price appreciation in secondary markets.

How long China will be able to avoid a sharp price decline remains to be seen, but in the meantime another problem faces China's housing market: in addition to being the primary source of household net worth - and therefore stable and growing consumption - it has also been a key driver behind China's economic growth, with infrastructure spending and capital investment long among the biggest components of the country's goalseeked GDP. One result has been China's infamous ghost cities, built only for the sake of Keynesian spending to hit a predetermined GDP number that would make Beijing happy.

Meanwhile, in the process of reflating the latest housing bubble, another dire byproduct of this artificial housing "market" has emerged: tens of millions of apartments and houses standing empty across the country.

According to Bloomberg, soon-to-be-published research will show that roughly 22% of China’s urban housing stock is unoccupied, according to Professor Gan Li, who runs the main nationwide study. That amounts to more than 50 million empty homes.

The reason for the massive empty inventory glut: to keep supply low and prices artificially elevated by taking out as much inventory off the market as possible. This, however, works both ways, and while it helps boost prices on the way up as the economy grow and speculators flood the housing market with easy money, the moment the trend flips the spike in supply as empty units are offloaded will lead to a panic liquidation of homes, resulting in what may be the biggest housing market crash ever observed, and putting the US home bubble of 2006 to shame.

Indeed, as Bloomberg notes, the "nightmare scenario" for Chinese authorities is that owners of unoccupied dwellings rush to sell when cracks start appearing in the property market, causing a self-reinforcing downward price spiral.

Worse, the latest data, from a survey in 2017, also suggests Beijing’s efforts to curb property speculation - which alongside shadow banking and the persistent threat of sudden bank runs (like the one discussed last week) is considered by Beijing a key threat to financial and social stability - have failed.

"There’s no other single country with such a high vacancy rate,” said Gan, of Chengdu’s Southwestern University of Finance and Economics. “Should any crack emerge in the property market, the homes to be offloaded will hit China like a flood.”

How did the Chinese researcher obtain this troubling number? To find the percentage of vacant housing, thousands of researchers spread out across 363 Chinese counties last year as part of the China Household Finance Survey, which Gan runs at the university.

Gan said that the vacancy rate, which excludes homes yet to be sold by developers, was little changed from a 2013 reading of 22.4%. And while that study showed 49 million vacant homes, Gan puts the number now at "definitely more than 50 million units."

Meanwhile, Beijing - which is fully aware of these stats, and is also aware that even a modest price decline could be magnified instantly as millions of "for sale" units hit the market at the same time - is worried. That's why Chinese authorities have imposed buying restrictions and limited credit availability, only to see money flooding into other areas. Rampant price gains also mean millions of people are shut out from the market, exacerbating inequality.

In fact, China's president Xi famously said in October last year that "houses are built to be inhabited, not for speculation", and yet a quarter of China's housing is just that: empty, and only serves to amplify speculation.

While holiday homes and the empty dwellings of migrants seeking work elsewhere account for some of the deserted properties, Gan found that investment purchases have been the biggest factor keeping the vacancy rate high. That’s despite curbs across the country meant to discourage buying of multiple dwellings.

There is another economic cost to this speculative frenzy: the drop in supply puts upward pressure on prices and crowds young buyers out of the market, according to Kaiji Chen, who co-authored a Fed paper called “The Great Housing Boom of China."

And, as Americans so fondly recall, the result of chasing unaffordable homes for the purpose of price speculation has resulted in yet another unprecedented debt bubble: according to Caixin, outstanding personal home mortgages in China have exploded sevenfold from 3 trillion yuan ($430 billion) in 2008 to 22.9 trillion yuan in 2017, according to PBOC data

By the end of September, the value of outstanding home mortgages had surged another 18% Y/Y to a record 24.9 trillion yuan, resulting in a trend that as Caixin notes, has turned many people into what are called “mortgage slaves."

It has also resulted in yet another housing bubble: home mortgage debt now makes up more than half of total household debt in China. As of the third quarter, it accounted for 53% of the 46.2 trillion yuan in outstanding household debt.

For now, few are losing sleep over what will be the next massive housing bubble to burst. An example of a vacant home is a villa on the outskirts of Shanghai that 27-year-old Natalie Feng’s parents bought for her. The two-story residence was meant to be a weekend escape for the family of three. In reality, it’s empty most of the time, and Feng says it’s too much trouble to rent it out.

"For every weekend we spend there, we need to drive for an hour first, and clean up for half a day," Feng said. She joked that she sometimes wishes her parents hadn’t bought it for her in the first place. That’s because any apartment she buys now would count as a second home, which means she’d have to make a bigger down payment.

* * *

What is troubling is that despite relatively stable home prices, the foundations behind the housing market are cracking. As the WSJ recently reported, in early December, a group of homeowners stormed the sales office of their Shanghai complex, "Central Washington", whose developer, Shanghai Zhaoping Real Estate Development, was advertising new apartments at a fraction of the prices of the ones sold earlier in the year. One apartment owner said the new prices suggested the value of the apartment she bought from the developer in March had dropped by about 17.5%.

“There are people who bought multiple homes who are now trying to sell one to pay off the mortgage on another,” said Ran Yunjie, a property agent. One of his clients bought an apartment last year for about $230,000. To find a buyer now, the client would have to drop the price by 60%, according to Ran.

Meanwhile, in a truly concerning demonstration of what will happen when the bubble finally bursts, last month we reported that angry homeowners who paid full price for units at the Xinzhou Mansion residential project in Shangrao attacked the Country Garden sales office in eastern Jiangxi province last week, after finding out it had offered discounts to new buyers of up to 30%.

Country Garden cut the selling price at one of its residential developments by 1/3. Those who paid full price smashed the sales office. Similar incidents had happened before, and will again. It’s impossible to remove “the guarantee of principal”(刚性兑付)in China.

"Property accounts for roughly 70 per cent of urban Chinese families’ total assets – a home is both wealth and status. People don’t want prices to increase too fast, but they don’t want them to fall too quickly either,” said Shao Yu, chief economist at Oriental Securities. "People are so used to rising prices that it never occurred to them that they can fall too. We shouldn’t add to this illusion," Shao added, echoing Ben Bernanke circa 2005.

But the biggest surprise once the music finally stops may be that - as a fascinating WSJ report revealed one year ago - China's housing downturn is likely far, far worse than meets the eye, as under Beijing’s direction more than 200 cities across China for the last three years have been buying surplus apartments from property developers and moving in families from condemned city blocks and nearby villages.China’s Housing Ministry, which is behind the purchases, said it plans to continue the program through 2020. The strategy, supported by central-government bank lending, has rescued housing developers and lifted the property market.

In other words, while China already has a record 50 million empty apartments, the real number - when excluding the government's own stealthy purchases of excess inventory - is likely significantly higher. It is this, and not China's stock market, that has long been the biggest time bomb for Beijing, and if Trump and Peter Navarro truly want to crush China in their ongoing trade war, they should focus on destabilizing the housing market: the Chinese stock market was, and remains just a distraction.

To summarize:

China has more than 50 million vacant apartments

Mortgage loans have grown 8-fold in the past decade

Prices are kept steady thanks to constant government purchases of surplus inventory

Home prices are already cracking, with some homebuilders forced to cut prices by 30%.

Homebuyers revolt, forming angry militias and storm homesellers' offices when prices dip

For now, China has been able to maintain the illusion of stability to preserve social order. However, should the housing slowdown accelerate significantly and tens of millions in empty units suddenly hit the market, then the "working class insurrection" that China has been preparing for since 2014...

... will become an overnight reality, with dire consequences for the entire world.

Analysts say a Chinese recession would only hurt the region. That may be wishful thinking...

When China finally has its inevitable growth recession – which will almost surely be amplified by a financial crisis, given the economy’s massive leverage – how will the rest of world be affected? With US President Donald Trump’s trade war hitting China just as growth was already slowing, this is no idle question.

Typical estimates, for example those embodied in the International Monetary Fund’s assessments of country risk, suggest an economic slowdown in China will hurt everyone. But the acute pain, according to the IMF, will be more regionally concentrated and confined than would be the case for a deep recession in the United States.

Unfortunately, this might be wishful thinking.

First, the effect on international capital markets could be vastly greater than Chinese capital market linkages would suggest. However jittery global investors may be about prospects for profit growth, a hit to Chinese growth would make things a lot worse. Although it is true that the US is still by far the biggest importer of final consumption goods (a large share of Chinese manufacturing imports are intermediate goods that end up being embodied in exports to the US and Europe), foreign firms nonetheless still enjoy huge profits on sales in China.

Investors today are also concerned about rising interest rates, which not only put a damper on consumption and investment, but also reduce the market value of companies (particularly tech firms) whose valuations depend heavily on profit growth far in the future. A Chinese recession could again make the situation worse.

I appreciate the usual Keynesian thinking that if any economy anywhere slows, this lowers world aggregate demand, and therefore puts downward pressure on global interest rates. But modern thinking is more nuanced. High Asian saving rates over the past two decades have been a significant factor in the low overall level of real (inflation-adjusted) interest rates in both the US and Europe, thanks to the fact that underdeveloped Asian capital markets simply cannot constructively absorb the surplus savings.

Former US Federal Reserve chair Ben Bernanke famously characterised this much-studied phenomenon as a key component of the “global savings glut”. Thus, instead of leading to lower global real interest rates, a Chinese slowdown that spreads across Asia could paradoxically lead to higher interest rates elsewhere – especially if a second Asian financial crisis leads to a sharp draw-down of central bank reserves. Thus, for global capital markets, a Chinese recession could easily prove to be a double whammy.

As bad as a slowdown in exports to China would be for many countries, a significant rise in global interest rates would be much worse. Eurozone leaders, particularly German Chancellor Angela Merkel, get less credit than they deserve for holding together the politically and economically fragile single currency against steep economic and political odds. But their task would have been well-nigh impossible but for the ultra-low global interest rates that have allowed politically paralysed eurozone officials to skirt needed debt write-downs and restructurings in the periphery.

When the advanced countries had their financial crisis a decade ago, emerging markets recovered relatively quickly, thanks to low debt levels and strong commodity prices. Today, however, debt levels have risen significantly, and a sharp rise in global real interest rates would almost certainly extend today’s brewing crises beyond the handful of countries (including Argentina and Turkey) that have already been hit.

Nor is the US immune. For the moment, the US can finance its trillion-dollar deficits at relatively low cost. But the relatively short-term duration of its borrowing – under four years if one integrates the Treasury and Federal Reserve balance sheets – means that a rise in interest rates would soon cause debt service to crowd out needed expenditures in other areas. At the same time, Trump’s trade war also threatens to undermine the US economy’s dynamism. Its somewhat arbitrary and politically driven nature makes it at least as harmful to US growth as the regulations Trump has so proudly eliminated. Those who assumed that Trump’s stance on trade was mostly campaign bluster should be worried.

The good news is that trade negotiations often seem intractable until the 11th hour. The US and China could reach an agreement before Trump’s punitive tariffs go into effect on 1 January. Such an agreement, one hopes, would reflect a maturing of China’s attitude toward intellectual property rights – akin to what occurred in the US during the late 19th century. (In America’s high growth years, US entrepreneurs often thought little of pilfering patented inventions from the United Kingdom.)

A recession in China, amplified by a financial crisis, would constitute the third leg of the debt super-cycle that began in the US in 2008 and moved to Europe in 2010. Up to this point, the Chinese authorities have done a remarkable job in postponing the inevitable slowdown. Unfortunately, when the downturn arrives, the world is likely to discover that China’s economy matters even more than most people thought.

Authored by Kenneth Rogoff, op-ed via The Guardian