“the slightest increase in interest rates could force them to decide whether to eat or pay their loan on their mobile home.” Here’s why it matters…

Some people in the United States have stopped paying their loans on mobile homes. This is a bad sign for the economy as many no longer can afford the increase in interest rates.

According to a report by Yahoo Finance, the mobile home market is showing the first signs of stress. The delinquency rate on mobile home loans has increased by 200 basis points, or 2 percentage points, over the past year, according to research cited by UBS. The 30-day-plus delinquency level is now about 5%, the highest level since 2005.

The increase in the number of struggling mobile-home borrowers suggests that a large chunk of these people haven’t benefitted from the economic growth of the past few years, despite the low unemployment level. For those living paycheck to paycheck, even the slightest increase in interest rates could force them to decide whether to eat or pay their loan on their home.

“We interpret this data to mean that these individuals have not largely benefitted from these macro-dynamics, and may also be disproportionately exposed to industries that have experienced compression — rather than expansion — in the current economic conditions, such as retail or some areas of energy extraction,” UBS said.

“The real choice is not between recession now or recession later. It’s between a massive recession now, or an even more devastating one later … Now is the time to bite the bullet, endure the pain, and allow the wound to actually heal,” said Schiff, who accurately predicted the 2008 recession and says the recovery isn’t a real one.

Since 2009, all of the standard metrics for indicating a recovery have shown sub-par results. The only growth has occurred in asset prices. However, higher prices in stocks and bonds haven’t occurred because of upward pressure from a free market, but have been artificially inflated by easy borrowing and risky speculation. Consequently, the “recovery” we’re supposedly experiencing is as artificial as asset prices themselves. The next bubble that will have to burst is the Fed’s own fantasy it’s been selling investors. –Schiff Gold

The truth is, the US economy is stuck; raising rates will send the US into a recession, but keeping them the same will make the eventual pain of an economic crash much worse. “I agree with those who believe that rate hikes now will bring on a recession,” Peter Schiff stated in an article. “But I disagree that we should keep rates where they are … despite the short term pain that will surely follow, we need to raise rates now to break the addiction before it gets worse.”

But UBS did admit that losses will start to impact other debts as well, and likely soon. “We believe weakness in these two groups [lower and middle class] will drive higher credit losses at some stage over the next few years — particularly in credit card, installment, and student loans — with macroeconomic inflection from job growth to job loss as a likely catalyst,” UBS said.

Now is a great time to prepare for the economic collapse. The economy won’t last forever being propped up by debt and Feds manipulation of the markets. But the good news is, prepping for the eventual collapse is made easy with the book titled The Prepper’s Blueprint. It’s a great resource for those just starting out and for those who may have overlooked something.

The Next Crisis Will Be The Last

It is an interesting thing.

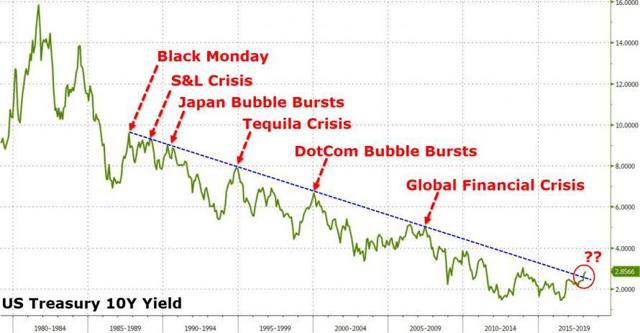

Throughout the last four decades there is a direct link between the actions of the Federal Reserve and the eventual economic and market outcomes due to changes in monetary policy. In every case, that outcome has been negative.

The general consensus continues to be the markets have entered into a “permanently high plateau,” or an era in which asset price corrections have been effectively eliminated through fiscal and monetary policy. The lack of understanding of economic and market cycles was on full display Monday as

“I’m thinking the smart money is certainly going to buy on the dips here because the economy is as strong as an ox.”

I urge you not to fall prey to the “This Time Is Different” thought process.

Despite the consensus belief that global growth is gathering steam, there is mounting evidence of financial strain rising throughout the financial ecosystem, which as I addressed previously, is a direct result of the Fed’s monetary policy actions. Economic growth remains weak, wages are not growing, and job growth remains below the rate of working age population growth.

While the talking points of the economy being as “strong as an ox” is certainly “media friendly,” The yield curve, as shown below, is telling a different story. While the spread between 2-year and 10-year Treasury rates has not fallen into negative territory as of yet, they are certainly headed in that direction.

This is an important distinction. The mistake that most analysts make in an attempt to support a current view is to look at a specific data point. However, when analyzing data, it is not necessarily the current data point that is important, but the trend of the data that tells the story. Currently, the trend of the yield curve is highly suggestive of economic growth not being nearly as robust as the mainstream consensus believes.

Furthermore, economic cycles are only sustainable for as long as excesses are being built. The natural law of reversions, while they can be suspended by artificial interventions, cannot be repealed. In a consumer based economy, where 70% of economic growth is driven by consumption, you have to question both what is driving consumer spending and how are they funding it. Both of those answers can be clearly seen in the data and particularly in those areas which are directly related to consumptive behaviors.

Stephanie Pomboy recently had an interview with Barron’s magazine in which she made several very salient points as it relates to current monetary policy and the next crisis. To wit:

” In January, the savings rate went from 2.5% to 3.2% in one month—a massive increase. People look at the headline for spending and acknowledge that it’s not fabulous, but they see it as a sustainable formula for growth that will generate the earnings necessary to validate asset price levels.”

Unfortunately, the headline spending numbers are actually far more disturbing once you dig into

“When you go through that kind of detail, you discover that they are buying more because they have to. They are spending more on food, energy, health care, housing, all the nondiscretionary stuff, and relying on credit and dis-saving [to pay for it]. Consumers have had to draw down whatever savings they amassed after the crisis and run up credit-card debt to keep up with the basic necessities of life.

When a bulk of incomes are diverted to areas

Despite the recent “windfall” from tax reform, corporations aren’t “sharing the wealth” as consumption trends remain weak. When revenue, what happens at the top line of the income statement, remains weak, corporations continue to opt for share buybacks, wage suppression and accounting gimmicks to fuel bottom lines earnings per share. The requirement to meet Wall Street expectations to support share prices is more important to the “C-suite” executives than being benevolent to the working class.

“Therefore, as the gap between the ‘desired’ living standard and disposable income expanded, it led to a decrease in the personal savings rates and increase in leverage. It is a simple function of math. But the following chart shows why this has likely come to the inevitable conclusion, and why tax cuts and reforms are unlikely to spur higher rates of economic growth.”

What the chart below shows is the differential between the standard of living for a family of four adjusted for inflation over time. What is clear is that beginning in 1990, the combined sources of savings, credit, and incomes were no longer sufficient to fund the widening gap between the sources of money and the cost of living. With surging health care, rent, food, and energy costs, that gap has continued to widen to an unsustainable level which will continue to impede economic rates of growth.

The Fed Will Do It Again

While it is currently believed that Central Bankers now have everything “under control,” the reality is they likely don’t. It is far more likely one of following two conclusions is more accurate.

The Fed is absolutely aware the economy is closer to the next recession than not. They also know that hiking interest rates in the current environment will likely accelerate the next downturn. However, the “lesser of two evils” is to face the recession with the Fed funds rate as far from zero as possible, or;

The Fed believes the economic data is indeed trending stronger and are overly confident in their ability to guide the U.S. economy into a “Goldilocks” type scenario where they can control inflationary pressures and growth rates to sustain a lasting economic cycle.

I agree with Stephanie’s point on how the next crisis will begin:

“Fed tightening continues to ratchet up and turns the screws on households and speculative-grade corporations, and the markets begin to anticipate more defaults, and reprice credit risk.”

Credit risk is already on the rise as consumers are much more sensitive to changes in rates. As the Fed continues to hike rates the negative impact on households will continue to escalate which is already showing up in credit card delinquencies.

Of course, it isn’t just credit card debt that is the problem. Subprime auto loans are pushing record levels as consumers have been lured into “cars they can’t afford” through low-rates and extended terms.

Consumers have also completely forgotten the last financial crisis and have once again turned to cashing out equity in homes to make ends meet.

Eventually, since a lot of this debt has been bundled up and sold off in the fixed income markets, this all ends badly when, as Stephanie states, the markets begin to reprice risk across the credit spectrum. As shown, when the spreads on bonds begin to blow out, bad things have occurred in the markets and economy.

For the Federal Reserve, the next “financial crisis” is already in the works. All it takes now is a significant decline in asset prices to spark a cascade of events that even monetary interventions may be unable to stem. As stock prices decline:

Consumer confidence falls further eroding economic growth

-

-

As prices fall, investors and consumers both contract further pushing the economy further into recession.

Aging baby-boomers, which are vastly under-saved will become primarily dependent on social welfare which erodes long-term economic growth rates.

With the Fed tightening monetary policy, and an errant Administration fighting a battle it can’t win, the timing of the next recession has likely been advanced by several months.

The real crisis comes when there is a “run on pensions.” With a large number of pensioners already eligible for their pension, the next decline in the markets will likely spur the “fear” that benefits will be lost entirely. The combined run on the system, which is grossly underfunded, at a time when asset prices are dropping will cause a debacle of mass proportions. It will require a massive government bailout to resolve it.

But it doesn’t end there. Consumers are once again heavily leveraged with sub-prime auto loans, mortgages, and student debt. When the recession hits, the reduction in employment will further damage what remains of personal savings and consumption ability. The downturn will increase the strain on an already burdened government welfare system as an insufficient number of individuals paying into the scheme is being absorbed by a swelling pool of aging baby-boomers now forced to draw on it. Yes, more Government funding will be required to solve that problem as well.

As debts and deficits swell in coming years, the negative impact to economic growth will continue. At some point, there will be a realization of the real crisis. It isn’t a crash in the financial markets that is the real problem, but the ongoing structural shift in the economy that is depressing the living standards of the average American family. There has indeed been a redistribution of wealth in America since the turn of the century. Unfortunately, it has been in the wrong direction as the U.S. has created its own class of royalty and serfdom.

The issue for future politicians won’t be the “breadlines” of the 30’s, but rather the number of individuals collecting benefit checks and the dilemma of how to pay for it all.

The good news, if you want to call it that, is that the next “crisis,” will be the “great reset” which will also make it the “last crisis.”

![[Chart]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_tWRU-5Hrjyg_cLNQJxJz9CMFgWyb1_79IqC7hDg4HrTryncgtBp_rUxS_nwF2gC-5w5mVuBSrOe4zyLVC0Eur3kh5pzJtir-QfueW_v0tzgVOpM_NE=s0-d)

![[Chart]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_twebWcIxZ3ZNyy4SYz06JtwNoZnj54qFb1QSch69IzP13HbabVonl8MAAZvxgklZo-Xryj2FGd4FqZ7D_-q-MDS2X78G7hXq9dpGswOYTYBtxZjSDtoA=s0-d)

![[Chart]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_va5QxEA4EkMimJ5I4Q7d44lsrd-suR3QYeHXPjVi7GRaOjfpNQaQPBd8OnC8dV3x7QcqHAJsXpb8fXwpaB6wA7mT4wije4YNpjb5fECErJNS6FMhQrJg=s0-d)